How Bridger Fund’s Waterfall Works: What Investors Actually Receive and Why

When a prospective investor evaluates a private real estate credit fund, they should understand how the economics flow, from the gross income of the fund down to an individual investor’s return. Most private real estate funds are equity funds in which investor returns are a function of capital appreciation and income generated by the property over a defined term. By comparison, for real estate debt funds, the return is a function of the interest rate and points paid by the borrower, which then flows through a waterfall distribution between the fund sponsor and the investor.

Capital appreciation or depreciation is usually not factored in unless the fund experiences a loan loss or a gain from a foreclosure. Because Bridger Fund’s loans generate interest income throughout their term, waterfall distributions flow to investors monthly. This is a meaningful contrast to equity real estate funds, where returns are typically realized at the sale of an asset — often years into the fund’s life. Investors at Bridger receive cash on a regular cadence as the portfolio performs.

In this article, we explain how Bridger Fund calculates its waterfall, using actual numbers from February 2026 as an example. We also address how other funds might differ in how they collect management fees and return value to investors.

What is a Waterfall?

A waterfall defines the order in which fund income is distributed. Income fills the first bucket, and only when that bucket is full does it flow to the next. Each tier has a defined recipient and rate, and a lower tier receives nothing until the tiers above it are paid in full.

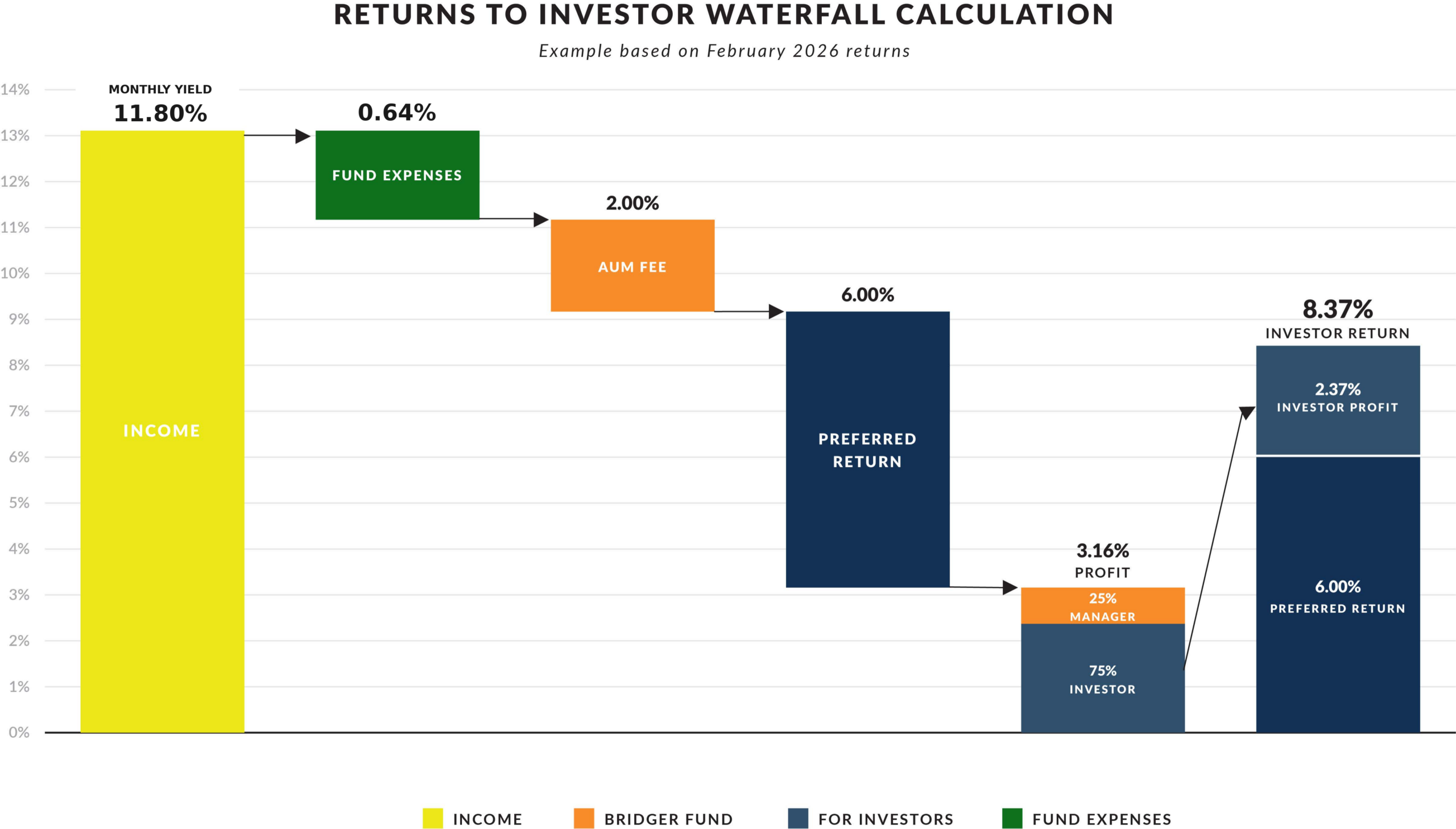

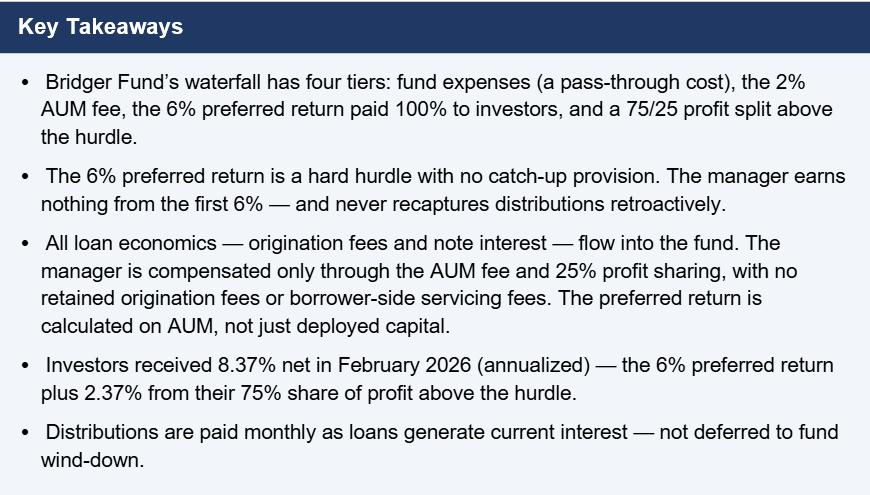

Bridger Fund’s waterfall has four tiers. The order matters: fund operating costs are covered first, and the management fee is paid second. Investors receive their full preferred return third, and only then does the manager participate in any profit sharing. The structure is straightforward, with both origination fees (points) and the note rate flowing to the fund. Bridger Fund is an income vehicle, so we think it is most illustrative to explain the waterfall in terms of annualized yield, so the investor can see how the percentage of total income flows down into the actual annualized return.

[Returns to Investor Waterfall Calculation — example based on February 2026 returns]

The Four Tiers, Explained

Tier 1: Fund Expenses (0.64%)

The first deduction covers the fund’s third-party operating costs — legal, audit, fund administration, and similar expenses required to run a fund vehicle. In February 2026, these expenses came to 0.64% on an annualized basis based on assets under management (AUM). These are pass-through costs, not manager revenue: they go to outside vendors. They come off the top because the fund must pay them regardless of how the loan portfolio performs.

Tier 2: AUM Fee (2.00%)

The second tier is Bridger Fund’s annual management fee, charged at 2.00% of assets under management. The AUM fee is the manager’s base revenue — it funds the team that originates, underwrites, and manages the loan portfolio, as well as other operating costs such as rent, technology, investor relations, and other administrative expenses. Unlike profit-share, it is a fixed percentage of AUM regardless of how the portfolio performs in any given month.

After the first two tiers, 3.94% has been deducted from the gross yield. The remaining 9.17% flows into the investor tiers below.

Tier 3: Preferred Return (6.00% — 100% to Investors)

The preferred return is a 6% priority distribution paid entirely to investors. The manager receives nothing from this tier. Until investors have been paid their full 6%, Bridger Fund earns no profit share.

The 6% is a floor, not a ceiling. In months where the portfolio earns more than 6% after expenses and fees, investors keep 75% of the excess through the next tier. The 6% preferred return is a hard hurdle, with no “catch-up.” In many private equity and private credit funds, the preferred return is paired with a catch-up provision. Once the hurdle is met, the manager receives 100% of subsequent distributions until it has caught up to its target carry percentage on total profit. Bridger Fund has no catch-up provision, an investor-friendly approach.

Tier 4: Profit Split (3.16% — 75% Investors / 25% Manager)

After the preferred return is fully paid, any remaining income is profit. In February 2026, that represented a 3.16% premium over the 6% hurdle. The split is broken down as 75% to investors and 25% to the manager:

- Investors receive 75% of 3.16% = 2.37% in additional return

- The manager receives 25% of 3.16% = 0.79% in profit sharing.

The Bottom Line: 8.37% Net to Investors

Finally, when adding the two investor tiers together – 6.00% preferred return + 2.37% profit share – that equaled a total return of 8.37% net to investors in February 2026, on an annualized basis.

How the Manager Gets Paid — and Alternative Structures

While most prospective investors focus on monthly returns, it is important to understand how fund managers earn their fees. In real estate private credit, fund sponsors collect manager compensation in several ways, and some of those structures create conflicts of interest or obscure where the manager’s economics actually come from. It is worth knowing the alternatives and how the Bridger Fund manager earns its fee.

Method 1: Manager keeps the loan origination fee

In this common structure, the manager originates loans and retains the origination fee directly — typically around 2% of the loan amount — while the fund (and therefore investors) only receives the loan’s interest rate less expenses. The conflict here is straightforward: the manager’s primary economic driver is loan volume, not loan quality or rate. There could be an incentive to originate as many loans as possible or try to win a deal by accepting a lower note rate, because the origination fee is the manager’s pay regardless of where the rate lands.

Method 2: A “servicing fee” embedded in the borrower’s rate

A second approach splits the manager’s fee between a smaller AUM fee—say, 1%—and a 1% loan-servicing fee charged directly to the borrower as part of the loan rate. A borrower expecting a 9% rate is actually paying 10%, with the extra 1% disclosed as a servicing fee that flows to the manager rather than to the fund. Borrowers tend to focus on the all-in rate they are paying, so this layering obscures rather than clarifies the economics. For funds that use leverage, this helps increase the manager’s income because a large part of the fee is based on the loan balance, including the leverage.

Method 3 (Bridger Fund’s Approach): All loan economics flow into the fund

This is the method Bridger Fund uses. Both origination fees and the note interest rate are paid into the fund. The manager does not retain a separate origination fee, and we do not add a hidden servicing fee to the borrower’s rate. All loan-level economics belong to the fund, and the manager is compensated only through the two mechanisms disclosed in the waterfall: the 2% AUM fee and the 25% carry on profit above the 6% hurdle.

One additional technical point is worth flagging: the 6% preferred return is calculated on AUM, not on outstanding loans. Some funds pay the preferred return only on actively deployed capital, meaning investors earn nothing on undeployed reserves between loan originations. Bridger Fund pays the 6% preferred return on the full investor capital base regardless of deployment status. Investors earn the priority return on every dollar they have committed.

The combined effect is a fee structure with no hidden levers: no incentive to chase loan volume over loan quality, no inflated borrower rates, and no meaningful gap between the portfolio’s gross yield and the income that flows into the waterfall. What you see in the four tiers is what is happening

A Note on Variability

The February 2026 example used here — 11.80% gross yield producing an 8.37% net investor return — reflects an actual month of fund performance. Monthly yields will vary based on portfolio composition, loan rates, cash deployment timing, loan payoffs, and default interest from loans past maturity. The waterfall structure itself does not change; what varies is the gross income flowing through it.

In months with lower gross yield, the preferred return remains the priority for investors after expenses and the AUM fee. It is the profit-sharing tier that compresses first — not the investor floor. In stronger months, investors capture the larger share of the upside through the 75% profit split above the hurdle.

To Learn More

If you would like to discuss how Bridger Fund’s structure fits into your portfolio — including current yields, allocation considerations, and the underlying loan portfolio — contact us at bridgerfund.com or through your Slatt Capital relationship.